Italy: not yet out of the woods?

During the time of uncertainty before a coalition of populist parties formed a government in Italy at the end of May, there was a rapid sell-off of Italian bonds, with the yield on the ten-year Italian government bond hitting 3.2 per cent in early June. In the same period, the Italian benchmark FTSE MIB index declined by 13 per cent compared to a month earlier.

Authors

During the time of uncertainty before a coalition of populist parties formed a government in Italy at the end of May, there was a rapid sell-off of Italian bonds, with the yield on the ten-year Italian government bond hitting 3.2 per cent in early June. In the same period, the Italian benchmark FTSE MIB index declined by 13 per cent compared to a month earlier.

At present, market stress has cooled down somewhat as the Minister of Finance has guaranteed not to breach EU fiscal rules and fears of an Italy-exit have faded.

That said, we are still far from an all-clear. In our August Economic Review we have revised down our forecasts for Italian GDP growth to 1.3 per cent this year and 1.2 per cent in 2019 This downward revision is on the back of the estimated medium-term impact of political uncertainty on confidence and investment plans, together with the deceleration in global trade observed in the first quarter reducing demand for Italian exports.

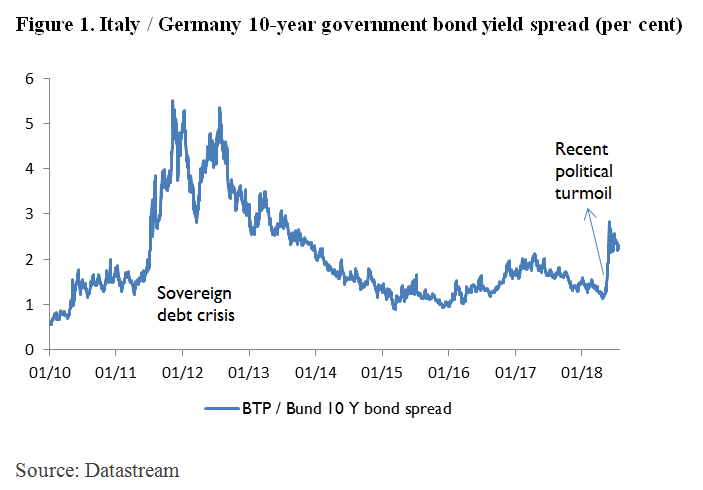

The domestic uncertainty is fuelled by the fragility of the coalition government, with the prospect of new elections not being yet far-off, and by doubts about the feasibility of its suggested reforms (as we discussed in a previous blog). On the basis of the movement in the bond yields spread (Figure 1), it looks like the recent political developments have rewound the clock to around mid-2013, the period when the adverse effects in markets originating from the sovereign debt crisis began to unwind.

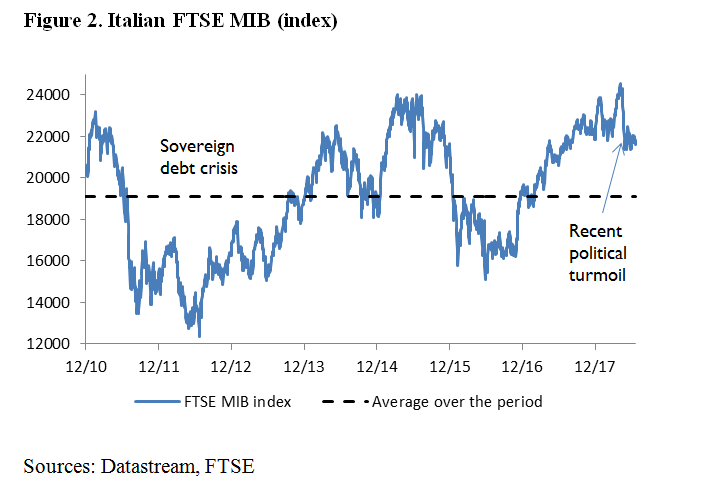

Looking at the equities market, the Italian FTSE MIB index performed robustly over 2017, recovering from the decline the year before. The upward trend halted and reversed quite sharply in early May this year, and Italian stock prices remain down by some 12 per cent today. Nonetheless, the fall in Italian share prices in this period looks mild when compared to the sharp and sustained sell-off in Italian shares during the sovereign debt crisis, which reduced the FTSE MIB price index by some 45 per cent by mid-2012 (Figure 2).

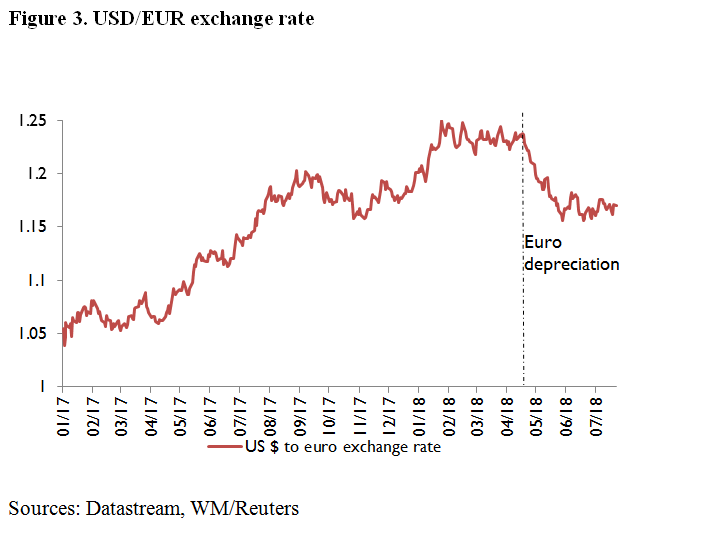

The euro appreciated against the dollar during last year on the back of an improved economic outlook across Euro Area countries, as well as a parallel increase of market turbulence in the US (Figure 3). In an article for the May Economic Review, Sophie Haincourt conducted an in-depth analysis of the causes of the exchange rate fluctuations in the US and Euro Area, and used NiGEM to simulate the effects of these fluctuations on key macroeconomic variables.

The appreciation of the euro, however, has reversed since April this year as the political turmoil in Italy and other events elsewhere have contributed to its depreciation, and the exchange rate remains now more than 5 per cent down compared to early April.

The post-war history of Italian politics shows that changes in government are relatively frequent. Since 1946, Italy has had 65 governments. By comparison, the UK and Germany have had only a third of such changes over the same period. This political instability is often reflected in financial markets. Although not of the same scale as in the 2011 crisis, the recent political surprises have led to market uncertainty and a heightened sense of risk. As of today, the market panic caused by the political developments seems to have calmed down. However, the political outlook in Italy still represents a source of major concern for markets, and so prospects for near-term growth and financial market stability indicate that we are not yet out of the woods.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum