The Local Economic Impacts of Brexit

Much has been written about the impact that Brexit might have on the national economy. We know far less about how that impact might vary across the UK. In a recent paper published in the National Institute Economic Review , myself and colleagues at the Centre for Economic Performance (Swati Dhingra and Steve Machin) provide some preliminary answers.

Authors

Much has been written about the impact that Brexit might have on the national economy. We know far less about how that impact might vary across the UK. In a recent paper published in the National Institute Economic Review , myself and colleagues at the Centre for Economic Performance (Swati Dhingra and Steve Machin) provide some preliminary answers.

The research looks at the difference in predicted effects across all Local Authority Areas under a ‘soft’ and a ‘hard’ Brexit scenario (the former involves zero tariffs, but increased non-tariff barriers with the EU, the latter involves non-zero tariffs and even higher non-tariff barriers). It also provides some initial analysis on whether these predicted impacts are likely to exacerbate or alleviate existing disparities and looks at how the predicted economic impacts of Brexit correlate with voting patterns from the referendum.

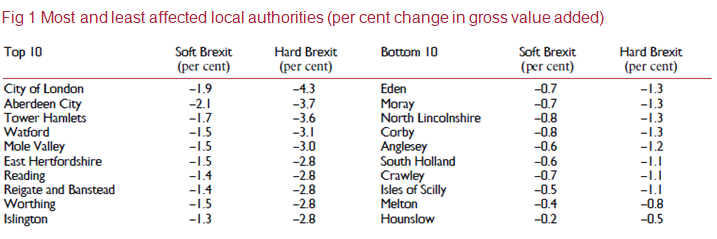

The results show that every local authority area is predicted to see a fall in GVA as a result of Brexit. The impacts are predicted to be more negative under ‘hard Brexit’ in every local authority area, as the increase in trade costs would be larger.

The report also suggests that in both scenarios, it is richer Local Authorities – predominantly in the South of England – which will be hit hardest and most directly by Brexit (Fig1). This reflects the fact that these areas specialise in financial and business services that are predicted to be hardest hit by the increase in tariff and non-tariff barriers that Brexit could bring. This pattern of results means that the predicted negative impacts are biggest for areas that tended to vote remain.

We aren’t yet able to model how those initial impacts will change as the economy adjusts. It’s quite possible that the places experiencing the biggest initial shock are not necessarily those that will experience the most negative effects once the economy has adjusted (we draw parallels with the financial crisis).

You can read more about all of these issues in the paper, so let me take the opportunity in this blog post to highlight my personal take on a few important issues:

– These are predictions relative to trend (i.e. what would have happened if the UK had stayed in the EU).

– We don’t take a stance on detailed institutional arrangements. Soft Brexit is ‘like a customs union’ – in that we assume zero tariff barriers and external tariff as now; but we take no position on changes in external tariff and who would decide on those.

– The model estimates medium to long run impact of changes in trade costs. We’re ignoring effects on innovation, immigration, inward investment, etc. We’re also ignoring adjustment. All of this should be clear from the report, but worth highlighting I think.

– Be careful on over interpreting the sector specific effects – particularly for industries like oil and air services where non-trade factors matter more. The technical paper has some discussion of the issues.

– The findings in which I have the most confidence are the general trends (1) bigger negative effects for areas specialised in services (setting aside any concerns about the exact sectoral predictions, we know non-tariff barriers and substitution away from UK supply will matter a lot for those sectors); (2) general north south pattern given those sectoral impacts; (3) correlation with vote remain (those predicted to be hardest hit voted to stay); (4) correlation with median wages (rich places hit worse); (5) once the economy adjusts things could look quite difference.

– I would avoid getting too hung up on exact rankings. These will change as analysis is refined, other factors added in, etc. (I realise that nothing I say here will stop people from doing this)

The figures in this paper represent a first attempt to look at the Local Authority impacts of the increases in trade barriers associated with Brexit. Further work will be needed to better understand these impacts, to understand the impacts working through other channels, such as migration and investment, and to understand the longer run impacts as the economy adjusts. In short, these figures are far from the last word, but they do provide an initial indication of the way in which the impact of Brexit may be felt differently across the areas of Great Britain.

Henry G. Overman is Professor of Economic Geography at the Department of Geography and Environment and Centre for Economic Performance, London School of Economics.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum