On US inflation now

Despite the headline CPI running at 5 1/2 percent in June and July, the 12-month trimmed mean PCE which excludes outliers is reported for June and July at 2 percent, and its monthly annualized rate fell from 3.1 percent in May to 2.4 percent in June, returning to 3.2 percent in July.

Authors

Despite the headline CPI running at 5 1/2 percent in June and July, the 12-month trimmed mean PCE which excludes outliers is reported for June and July at 2 percent, and its monthly annualized rate fell from 3.1 percent in May to 2.4 percent in June, returning to 3.2 percent in July.

.JPG)

This measure is the closest published to the “trimmed volume” measure which I argued in an earlier NIESR Policy Paper is the optimum measure of underlying inflation across a pandemic.

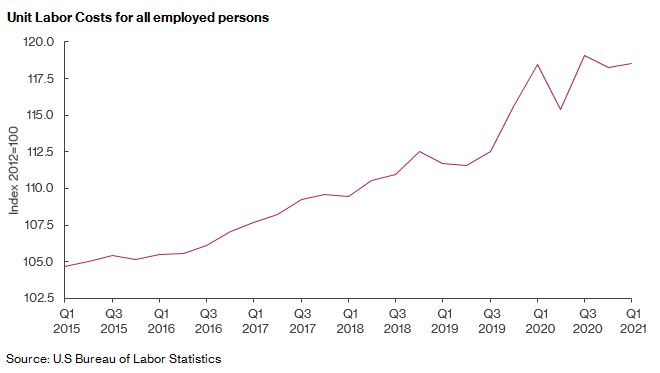

Alongside, underlying trends in unit labor costs remain benign, and frequent assertions that labor force participation is being distorted by income support have found no technical confirmation.

All this indicates substantial scope for labor force participation to rise back at least to immediate pre-pandemic levels if not considerably further.

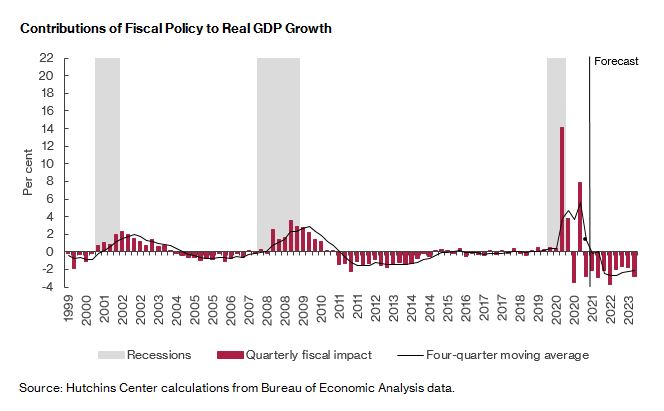

And the Brookings Hutchins Center reports that the “unless Congress Acts” fiscal policy for 2022, for consolidated Federal, State, and local Government, is an unprecedented contraction of some 3 percentage points of GDP, which has already begun. This will be compounded by the staggered expiry of eviction and other moratoria.

So, despite the drumbeat of inflationary alarums, is the prospect for 2022—on standard views of the sign and size of fiscal multipliers, and once base effects pass out in coming months—underlying disinflation from 2 percent or even underlying deflation, whatever price outliers do to the various headline and core measures of inflation from here on?

The implicit rebuttal of this view sees pandemic as binary. Given vaccines, US pandemic is over, so personal savings rates will not only drop from pandemic peaks, but will fall well below pre-pandemic rates as consumers run down “excess stocks of savings” accumulated in pandemic. So the default fiscal contraction merely—and pseudo-automatically—reflects the switch of pandemic from 1 to 0, with multipliers of approximately zero.

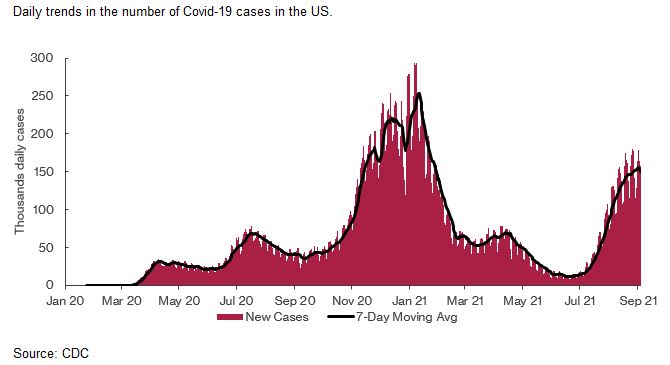

But this implicit rebuttal does not withstand scrutiny. Personal savings rates post fiscal stimulus and prior to full US Delta remain above pre-pandemic levels—even rising from June to July—as both theory and past behavior anticipate; and Delta and prior Greek lettered variants makes a mockery both of the binary assumption and of the presumption that the benevolent binary switch has occurred.

No epidemiologist ever said that pandemic was binary. But that assumption underpins the apparently unshakable grip that V-shaped recovery has on some economists’ thinking about pandemic.

Instead, the macroeconomic issue is that pandemic is not binary and that the US fiscal contraction is largely determined by law or/and politicians, not by direct reference to economic activity—it does not reflect the operation of automatic stabilizers. So if pandemic persists, via Delta or subsequent Greek lettered variants, US fiscal contraction takes place, by default, anyway.

That—abstracting from price outliers—is a recipe for disinflation from 2 percent, if not deflation.

So if we set aside the chest-thumping macroeconomic warnings and arise from our armchairs to put ourselves in the FOMC’s shoes, what is it to do now?

- As the pre-pandemic standard macroeconomic answer held, it should assume the default announced fiscal policy until that is formally changed.

- That injunction includes infrastructure because both bills remain hostage to razor thin margins in both houses of Congress—with House deal for a September 27th vote on the smaller bill stacking the cards against the more ambitious lobby. And even if both bills eventuate in some form, some is spending merely reallocated within the default fiscal path, some is deficit neutral due to genuine pay-fors, and both decadal programs are, inevitably and anyway, backloaded.

- Similarly, with policy interest rates near the effective lower bound, the FOMC should weigh downside risks to activity higher than the upside because it is fully instrumented to address the latter, and at speed, but not the former, and fiscal flexibility will be cut in 2022, an election year.

- And given monetary policy lags, the FOMC has to take a view on the outlook for the pandemic—beyond that it just forced the Jackson Hole conference to go virtual again. This judgement should reflect often counterproductive policy (see Florida, the premature withdrawal of the mask mandate in May, non-systematic testing, and ongoing vaccine nationalism), eroding vaccine immunity, and a big element of chance—all of which the “V-recovery” assumption simply ignores.

On this basis, the question is not whether the FOMC will be behind the curve or not as if that curve is already binarily determined; it is which policy mistake should the FOMC prioritize avoiding now?

In answering, an explicit policy call is required:

- underlying inflation, if it rises as pandemic ends, can be fixed even if at the expense of a sharp tightening;

- but a crunching recession and disinflation or deflation if pandemic persists would be catastrophic, given the lower effective bound and Congressional fiscal logjam in 2022.

So disregarding any calendar triggers, until:

- personal savings rates fall below pre-pandemic levels;

- underlying nominal wage growth destabilizes; and

- above-target inflation shows up in trimmed mean PCE excluding base effects,

the FOMC should disregard the drumbeat—however insistent, well-intentioned, or imaginative—of inflation alarums, and retain current monetary policy stimulus. The policy reactions outlined by Fed Chair Powell in his Jackson Hole address are appropriate, but only when these conditions are met

Further, with immediate effect, the FOMC should advance by two weeks the monthly publication of the trimmed mean PCE to the same day as the CPI release. This would significantly improve effectiveness at communicating the diagnosis of headline inflation as transitory and so help to check a fortnight of hyperbolic speculation every month about the implications for monetary policy of the CPI.

And finally, policymakers should urgently set about changing the default fiscal policy—including steps for the big infrastructure stimulus—lest a very different stance from default is needed in 2022 and beyond.

Accordingly, even if pandemic ends swiftly and underlying inflation emerges and has to be checked, that would not mean that this counsel was wrong—unless inflation alarmist economists wish in hindsight to claim to have possessed a clairvoyance in their unconditional forecasts of pandemic which now utterly eludes epidemiologists.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum