Resilient to the Challenges of the New Reality

The global economy has shown resilience to tighter monetary policies and geopolitical challenges, but GDP growth slowed to around 3 per cent in the past two years. We expect outlook for both advanced and emerging economies to remain lacklustre and forecast global GDP to grow by 3.1 per cent in 2024 and 3.2 per cent in 2025.

Sign in to Access Pub. Date

Pub. Date

09 May, 2024

Pub. Type

Pub. Type

Authors

External Authors

Main points

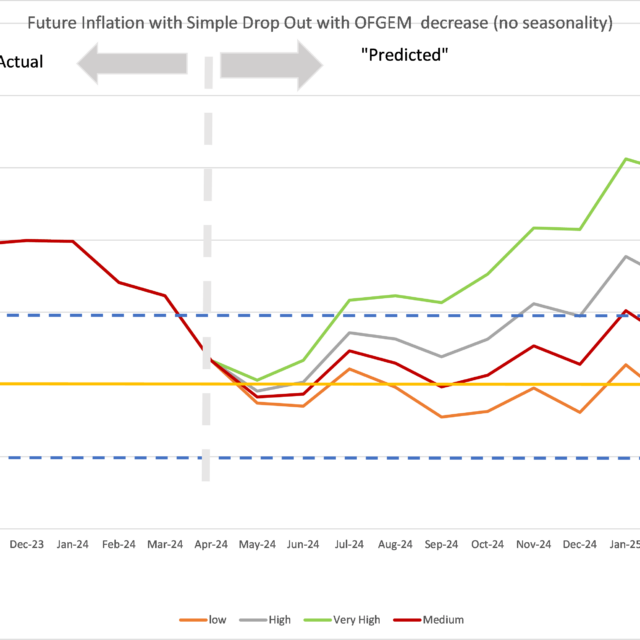

- Despite significant falls in headline inflation in advanced economies, thanks to tighter monetary policies and lower commodity prices, core inflation remains elevated. We forecast that OECD annual inflation (excluding Turkey) will fall from 5.9 per cent last year to 3.8 per cent in 2024 and 1.8 per cent in 2025.

- With inflation falling steadily and economic activity stagnant, we expect the European Central Bank (ECB) to start interest rate cuts in June. The Federal Reserve (Fed) may delay rate cuts until September due to stickier inflation in the United States. We expect further reductions through next year as inflationary pressures continue to weaken.

- Rising interest rates, particularly government bond yields, have put pressure on fiscal balances in advanced economies. Increased costs of debt service leave governments with little room for positive fiscal policy actions in 2024 and 2025 at a time when government debt levels are already running at high shares of GDP.

- Continued uncertainty due to war in Ukraine and tensions in the Middle East poses considerable risks to economic activity and inflation. Our forecast and revisions since our Winter Global Economic Outlook are summarised in table 1 and our fan charts for global GDP and (OECD) inflation are shown in figures 1 and 2.

Related Blog Posts

Related Projects

Related News

Related Publications

publication

A Macroeconomic Analysis of the Main Parties’ Spending Pledges

24 Jun 2024

General Election Briefing

Related events

Summer 2023 Economic Forum

11:00 to 12:00

11 August, 2023

Spring 2023 Economic Forum

11:00 to 12:00

12 May, 2023

Winter 2023 Economic Forum

11:00 to 12:00

10 February, 2023

Autumn 2022 Economic Forum

11:30 to 12:30

18 November, 2022

Summer 2022 Economic Forum

11:00 to 12:00

5 August, 2022

Spring 2022 Economic Forum

11:00 to 12:00

13 May, 2022

Winter 2022 Economic Forum

11:00 to 12:00

11 February, 2022

Autumn 2021 Economic Forum

11:00 to 12:00

12 November, 2021