Fiscal policy, “Plan A” and the recovery: explaining the economics

Does the UK recovery prove wrong those of us who argued that the Government's fiscal consolidation plan, announced in June 2010, was poorly designed and ignored some basic economic principles? The Chancellor, not surprisingly, says yes:

Authors

Does the UK recovery prove wrong those of us who argued that the Government’s fiscal consolidation plan, announced in June 2010, was poorly designed and ignored some basic economic principles? The Chancellor, not surprisingly, says yes:

Proponents of the ‘fiscalist’ story cannot explain why the UK recovery has strengthened rapidly over the last six months. The pace of fiscal consolidation has not changed, government spending cuts have continued as planned, and yet growth has accelerated and many of the leading economic indicators show activity rising faster than at any time since the 1990s. If the fiscal multipliers were much higher than the OBR estimates, as the fiscalist story requires, this should not be possible. Indeed, proponents of the fiscalist analysis predicted that stronger growth would only return if the government changed course and reduced the structural pace of consolidation.

On the other side, there are two main points, made here. by Paul Krugman:

First of all, Britain’s recent growth doesn’t change the reality that almost six years have passed since the nation entered recession, and real G.D.P. is still below its previous peak. Taking the long view, that’s still a story of dismal failure — as I said, a track record worse than Britain’s performance in the Great Depression.

Second, it’s important to understand the history of austerity in Mr. Osborne’s Britain. His government spent its first two years doing big things: sharply reducing public investment, increasing the national sales tax, and more. After that it slowed the pace; it didn’t reverse austerity, but it didn’t make it much more severe than it already was.

And here’s the thing: Economies do tend to grow unless they keep being hit by adverse shocks. It’s not surprising, then, that the British economy eventually picked up once Mr. Osborne let up on the punishment.

So which of these stories makes sense? This is where it gets complicated. There are actually several separate questions here:

a) does the current recovery show, as the Chancellor argues, that those who claimed fiscal multipliers were large were wrong?

b) did fiscal consolidation in fact slow down?

c) and did the government stick to its Plan A, or did it move to Plan B sometime in 2012 or so?

Let me take these in turn.

a) What does the recovery tell us about fiscal multipliers?

Here the answer is actually rather clear, and is shown in this chart from the Office of Budget Responsibility.

.jpg)

This shows the OBR’s estimate of the impacts of fiscal consolidation on the level of GDP. The OBR thinks consolidation reduced GDP by about 1.5%, with almost all that impact feeding through by 2012. Now, of course, Krugman and others argued all along that the multipliers were in fact larger, and hence the impact more negative. Well, suppose we were right, and – for the sake of argument – the multipliers were in fact twice as big. In that case, the negative impact on GDP would have been about 3%. But again, almost all that impact would have been seen by 2012 – all you would do to the OBR’s chart is double the size of the bars. What would bigger multipliers imply for growth now? Well, in fact, the chart suggests that the OBR thinks fiscal consolidation is now having a (very small) positive impact on growth. So if the multipliers are in fact bigger than the OBR thinks, that small positive impact would be larger. As Simon Wren-Lewis put it

In the textbook case austerity implies a deeper recession but then a subsequent recovery that is stronger as a result. So in that case rapid growth provides evidence in favour of the ‘fiscalist’ case, not against it.

So the Chancellor is flat wrong, at least if you think the OBR is reasonably close to being correct about the timing of the impacts of consolidation. That doesn’t mean, in this particular case, that larger fiscal multipliers can explain the current recovery – it just means that those who argue that the recovery supports the view that multipliers are small simply don’t understand the basic economic concepts here. .

b) Did consolidation in fact slow down?

Here the question is rather different – not about the size of multipliers, but the size of the consolidation to which multipliers should be applied to. And here, of course, matters are complicated by the fact that there are several different ways of measuring fiscal consolidation.

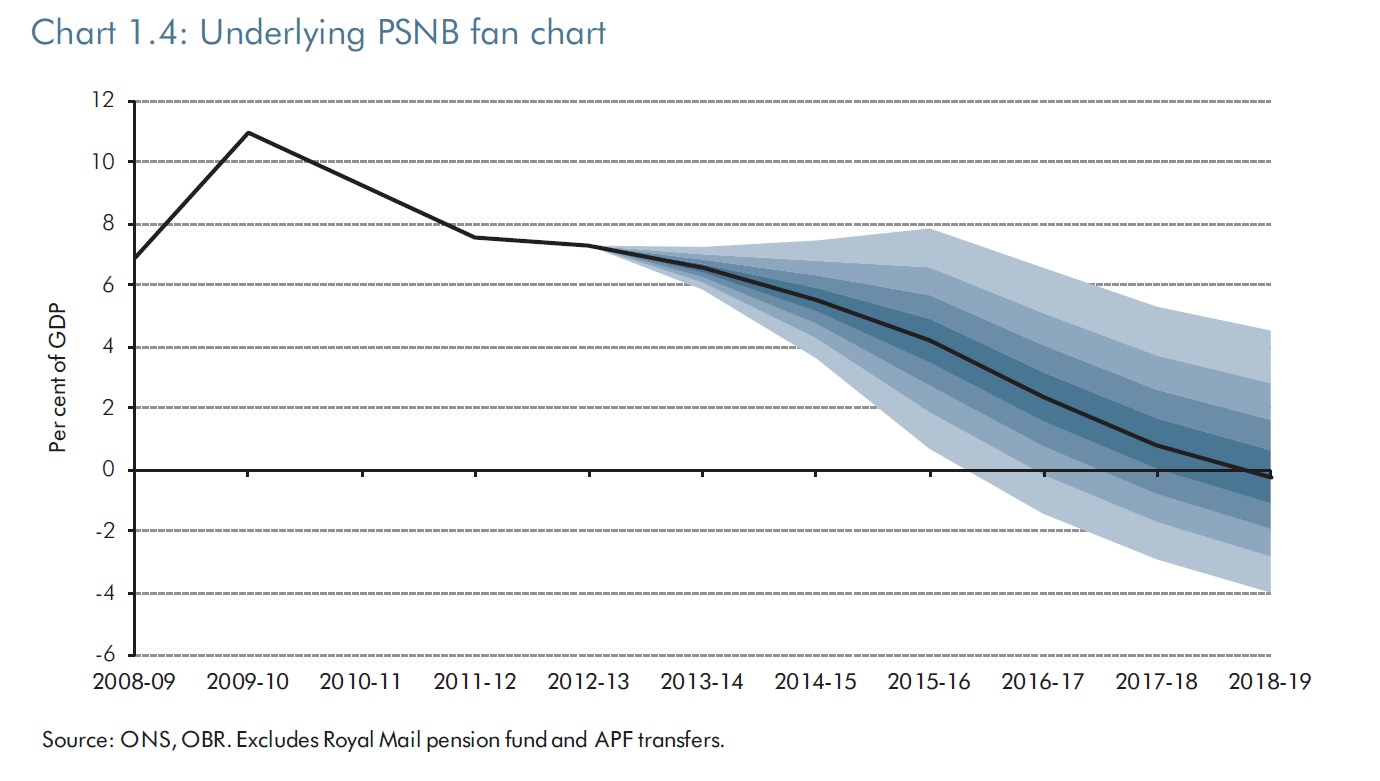

The simplest, and most obvious, is to look at the size of the deficit. This OBR chart really needs little commentary, except to say that it is not exactly consistent with the Chancellor’s claim that “the pace of fiscal consolidation has not changed”, but is rather closer to Robert Chote’s view that “deficit reduction appears to have stalled”.

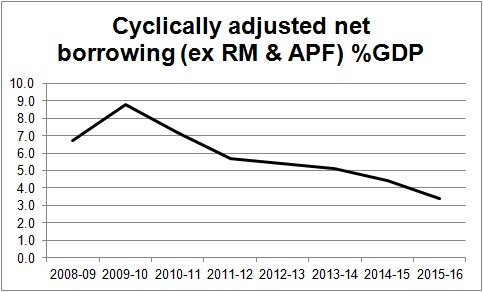

However, most economists, and the government, prefer to look at the “cyclically adjusted” , or “structural” deficit. This makes much more sense as a measure of consolidation, since it takes account of the fact that of course the deficit goes up if the economy gets worse. Unfortunately the OBR don’t publish a chart for their preferred measure – cyclically adjusted borrowing excluding the distortions resulting from the Royal Mail pension fund transfer, and the accounting treatment of the revenues in the Asset Purchase Fund. But it can easily be constructed from their data, so here it is:

Same story. Sharp consolidation up to 2012, then “stalled”. Now, the Treasury’s response to this is to claim that the data show “a gradual and relatively steady reduction in the estimated structural deficit.”

Well, obviously it depends what you mean by “steady”. Or perhaps what you mean by “relatively”. But I think we can treat this assertion with the seriousness it deserves. More detail on this from Simon Wren-Lewis here.

[UPDATED: In his speech today, the Chancellor doubled down on this line, saying

The pace of our fiscal consolidation over the last four years has been steady, with an average annual reduction in the cyclically adjusted primary balance of around 1.6% of GDP according to the IMF – the largest and most sustained of any major advanced economy.

Leaving aside the question of why the Chancellor is using IMF figures rather than those of the OBR – the body he himself set up to be the authoritative judge of the UK fiscal position – this is, shall we say, disingenuous. The IMF figures actually show a reduction in the cyclically adjusted deficit of 2.5% in 2011. In 2012 the reduction was 0.2%. But the Chancellor says the pace was “steady”. Does he really think anyone is gullible enough to believe this?]

[The Treasury also point out that estimating the structural deficit is very difficult; estimates vary and change, and the IMF and OECD have quite different numbers. This is absolutely right but begs two obvious questions. First, if that’s the case, why is the structural deficit (as estimated by the OBR) the official government target (see below)? And second, although the IMF and OECD estimates are different, partly because they treat the RMPF/APF distortions differently, their estimates also show fiscal consolidation slowing significantly after 2012; in neither case could the reduction in the structural deficit be described as “relatively steady”. So this is more an attempt to obfuscate than a serious counter-argument].

c) Did the government ditch Plan A?

Here we move, at least in part, from economics to politics, or at least semantics. In my view, Plan A was the government’s Fiscal Framework/fiscal mandate, as set out very prominently in the 2010 Emergency Budget.

The Budget announces the Government’s forward-looking fiscal mandate to achieve cyclically-adjusted current balance by the end of the rolling, five-year forecast period. At this Budget, the end of the forecast period is 2015-16. At this time of rapidly rising debt, the fiscal mandate will be supplemented by a target for public sector net debt as a percentage of GDP to be falling at a fixed date of 2015-16, ensuring that the public finances are restored to a sustainable path.

This fiscal mandate, supplemented by the target for debt, will guide fiscal policy decisions over the medium term, ensuring that the Government sets plans consistent with accelerating the reduction in the structural deficit so that debt as a percentage of GDP is restored to a sustainable, downward path.

So plans were to be set consistent with “accelerating the reduction in the structural deficit”, with a view to eliminating it by the end of 2015-16, and for debt to be falling (relative to GDP) by 2015-16. So relative to what the government actually said its fiscal policy was, the answer is unequivocal: Plan A was ditched in 2012, as I said at the time.

But the Treasury now claim that the government’s (much vaunted at the time) “fiscal mandate” wasn’t Plan A at all. Instead, Plan A was simply the list of fiscal consolidation measures (the VAT rise, benefit cuts, etc) announced in 2010; and these have indeed been implemented. As the Chancellor puts it: “government spending cuts have continued as planned”.

I find this very odd, at least from an economic perspective. Is the Treasury claiming that the slowdown in the reduction in both the absolute and structural deficits was planned all along? I think not. Are they claiming there have been no changes to tax or spending policy since 2010? Ditto. Were the cuts to public investment (implicit in the plans of the previous government, but implemented by this one) part of Plan A? What is the economic significance of not implementing something which never existed except on paper? (the spending plans of the previous government). As I said, this becomes semantics, not economics.

Chris Giles is a particularly strong proponent of this argument, putting it forcefully just yesterday:

Those claiming Mr Osborne ditched austerity last year should quantify which departments, benefit recipients or taxpayers were given extra spending power last year. It simply did not happen.

Well, OK, here’s the OBR again, in their Budget analysis:

We have made various estimating changes to our forecasts, in particular for Employment and Support Allowance…We have increased the assumed caseload because the latest evidence suggests that the caseload is higher than we assumed in December, despite substantial upward revisions made at that time. We have updated the modelling on repeat Work Capability Assessments.. meaning more claims continue for longer.

In other words, the current mess surrounding Work Capability Assessments – the accelerated roll out of which was announced in 2010 and was supposed to deliver large savings – has meant those savings aren’t materialising, forcing the OBR to change its projections for benefit spending. This means, to use Chris’s own words, “benefit recipients” were “given extra spending power. ” Now, of course, there are dozens of other changes to the original policies announced in 2010, going in different directions; it’s close to impossible to make sense of it all and say whether “Plan A”, in this sense, remains. But that just illustrates why the simpler, and more economically coherent, measures of the fiscal stance described in b) above are more appropriate.

Finally, one, mostly rhetorical, point made against me and others is “well, if all this is true, why were you so vocal in opposing government policy through 2013, and why didn’t you predict the strong recovery we’re seeing now”?

There is some truth in this. We were slow to realise what was really happening, a point made by Simon Wren-Lewis here. Although, as noted above, I pointed out in 2012 that Plan A was dead, I didn’t realise the significance of that, combined with the arithmetic implications of the fading out of the impact of the multipliers – although it’s all in this August 2012 article, by me and others, if you read it properly! (see Figure 9 here (£)).

And almost all economists, certainly including me, underestimated the strength of the recovery. But, as shown in a) above, that had nothing to do with getting it wrong in on fiscal policy – it was much more to do with a combination of exogeneous factors (developments in the eurozone, etc) with the strength of the UK housing market and the associated pickup in consumer spending. More here.

Related Blog Posts

Related Projects

Related News

Letter to the Financial Times: Is Perfidious Albion About to Make a Return?

14 Jun 2024

3 min read

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Everything You Wanted to Know About the US Budget Deficit and Debt But Were Afraid to Ask

09 May 2024

Global Economic Outlook Box Analysis

To What Extent Has the Recovery and Resilience Facility Supported the EU Recovery from Covid?

09 May 2024

Global Economic Outlook Topical Feature

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

Related events

2024 UK General Election: The Economy and Living Standards

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum