Friday Flyer: The 2017 Election Result: where are we going?

The hung Parliament is a vote for ‘None of the above’. Sadly, none of the political parties addressed the economic issues that have dominated the experiences of households over the past 10 years. Productivity has barely progressed in a decade and as a result real wages have hardly increased either.

Authors

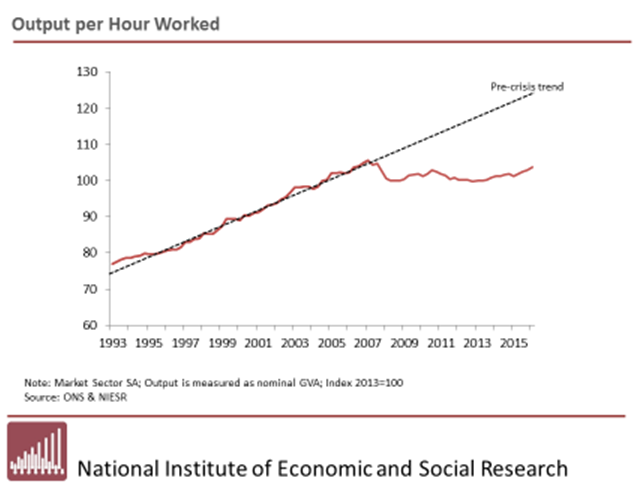

The hung Parliament is a vote for ‘None of the above’. Sadly, none of the political parties addressed the economic issues that have dominated the experiences of households over the past 10 years. Productivity has barely progressed in a decade and as a result real wages have hardly increased either. The figure below illustrates the underperformance of productivity relative to what households whose incomes are closely related to worker output per hour might have anticipated in 2007. We are now some 15-20% below those expectations and the sequence of elections and referenda we have had reflect to some great degree those frustrated expectations. Remember that I am showing here average productivity so many households have done even worse.

The UK economy continues to face a number of critical problems. The mix of capital to labour is too low to allow sufficiently high growth in real wages. This outcome, whilst it limited the impact of the Great Recession on unemployment, also limited the growth in productivity in the recovery and has the potential to increase income inequality over time. That said the vulnerability of the household sector to income shocks has been cushioned in aggregate by a large increase in net wealth in housing and equity. But arguably too much of debt and asset accumulation is tied up with property, which leave households vulnerable to an adjustment in property prices and also may lead to the creation of significant price-based barriers to entry to the housing market: these entry barriers reduce the prospects for economic mobility . The concentration of assets in housing rather than equities or fixed income funds may also act to limit the availability of loanable funds.

Furthermore, the regional disparities in productivity and income are also reflected in the evolution in house prices which may further hamper growth by limiting labour mobility. Monetary and fiscal policies could in principle act to offset some of these distortions but they may be close to the limits of their operating scope with interest rates at zero and public debt around 90% of GDP. All of these factors may imply a need to rethink the jointly determined objective for monetary- fiscal and financial policy.

The conventional wisdom was that this election was about the UK’s decision to leave the EU and this is clearly a critical question. But since the referendum was called in February 2016 and in the year since the Leave vote no-one has explained clearly how we intend to depart the European Union. The case for some clarity is now urgent. Rather than using silence on our key objectives as a way to negotiate it might better to be clear about what we wish to achieve with our long-standing political and economic partners in Europe. To the extent that the Brexit negotiations use up our public policy making capacity there is a danger than the urgent will drive out the important. Because now more than ever political parties should not shy away from facing the question of Britain’s underlying economic weakness and should be called upon to offer solutions that address the lost decade of economic growth the country has endured.

The issues of underinvestment, regional imbalances, an infrastructure gap and a hampered financial sector combined with a housing shortage continue to undermine the performance of the UK economy. At the Institute we provided a number of briefings on these issue because we are looking for answers from our political leaders. The political parties have in turn not given those answers in their manifestos and so the people may have just asked them to try again please in another election. And yet the clock on the negotiations to leave the European Union has started. We don’t have much time.

Related Blog Posts

How the Chancellor’s Budget Could Help Households and the Struggling Regions

04 Mar 2024

6 min read

Related Projects

Related News

Related Publications

Geopolitical Risks and the Global Economy

07 Feb 2024

Global Economic Outlook Box Analysis

Adam Smith and the Bankers: Retrospect and Prospect

04 Jan 2024

National Institute Economic Review

On the Promises and Perils of Smithian Growth: From the Pin Factory to AI

04 Jan 2024

National Institute Economic Review

Related events

What Can Policy Makers Learn From Adam Smith?

NMITE and the Political Economy of Higher Education – Jesse Norman

Economic Effects of Russia’s Invasion and Sanctions

2022 Deane-Stone Lecture – The Uses and Abuses of Economic Statistics

The Political Economy of Devolution in, and Secession from, the UK