The triple lock on pensions: An urgent case for change?

This is a guest blog by Richard Disney, Professor of Economics at the University of Sussex, A Visiting Professor in the Department of Economics, University College, London, and a Research Fellow of the Institute for Fiscal Studies.

This is a guest blog by Richard Disney, Professor of Economics at the University of Sussex, A Visiting Professor in the Department of Economics, University College, London, and a Research Fellow of the Institute for Fiscal Studies.

The so-called ‘triple lock’ on the state pension continues to command attention and criticism. Under the triple lock, introduced in 2010, there is a statutory requirement to increase (‘uprate’) the state pension each year at the highest rate of the rate of growth of prices or earnings or by not less than 2.5%. Analysts, ranging from the Director of the Institute for Fiscal Studies to the more partisan Institute of Economic Affairs, have called for the abolition of this triple lock to pension increases on grounds of future cost. The Government Actuary’s Department, in a briefing note subsequently withdrawn, also called into question the triple lock for similar reasons. Recently, such influential voices have been joined by the recently-departed Minister of Pensions, Baroness Altmann and, implicitly, by the Director of the Office of Budget Responsibility, Robert Chote, who has declared the policy ‘unsustainable’.

My own view, amplified in this note, is that, while it would be foolish of the current government to rule out any future review of the ‘triple lock’ (indeed it has not done so), there are other priorities in terms of economic policy that are more pressing in the current Parliament.

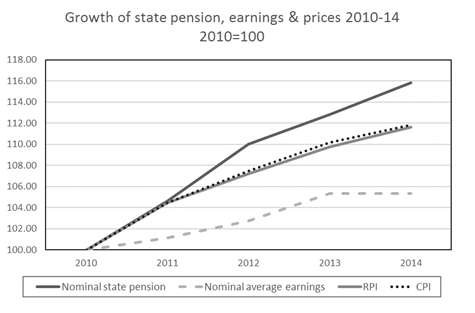

The reason for the concerns about the effect of the ‘triple lock’ are straightforward. As the graph shows, since 2010 the growth of the state pension has outstripped earnings growth, and any standard measure of inflation, by a significant amount. This is wholly due to the ‘third leg’ of the ‘triple lock’ – the minimum uprating of 2.5% per annum. If the basic state pension had risen at the rate of real earnings growth since 2010, it would now be worth around £15 a week less than its current value. If it has risen at the rate of inflation, it would be at least £5 a week less.

The reason for this disparity, of course, is the unprecedentedly slow growth (from a recent historic perspective) of prices and earnings since the ‘Great Recession’ that engulfed the UK economy in 2008. So, the critics argue, if the current trajectory of prices and earnings growth continues for any length of time, pensioners will forge further ahead of other groups in the economy, especially workers. This may be both financially unsustainable, since pension increases are financed out of current taxation, and ‘unfair’ to younger generations who have, it is argued, borne the brunt of the Great Recession in the form of lower earnings and difficulties in accessing capital, especially getting on the home-ownership ladder.

History suggests pension indexation arrangements are not set in stone

Before considering these arguments for scrapping the ‘triple lock’, it is worth delving into a little history. The policy for uprating the state pension has varied from decade to decade and has rarely been settled for any prolonged period. In the 1960s, early 1970s and 1980s, when the basic state pension was indexed to prices or erratically uprated on an ad hoc basis, pensioner incomes fell behind those of workers. In the late 1970s, uprating was undertaken on a ‘double lock’ of the highest of prices or earnings. In the more recent period, indexation was sometimes linked to earnings growth. These and other frequent changes in UK pension policy are described in Disney (2016).

However, an important complication to this ‘story’ of changes to pension uprating is that the state pension programme from 1962 to 2014 contained a multitude of ‘tiers’ or ‘pillars’ including an earnings-related component, as well as means-tested benefits and other additions such as specific benefits (e.g. the Winter Fuel Allowance). And the different benefits, as well as the various floors and ceilings that governed benefit entitlements such as the National Insurance Lower and Upper Earnings Limit, have typically been indexed by different criteria. For example, the basic pension might be uprated in line with earnings whereas the ceiling on and payments of earnings-related additions would only indexed to prices. Or the basic pension would be indexed to prices whilst means-tested benefits such as the Pension Credit were indexed to earnings. A consequence of these complexities (which were particularly apparent in the decade after 2000) was that any particular generous component of the programme (in terms of indexation) tended to substitute for a less generous component in the total pension entitlement. This effectively ‘dampened’ the total cost of the programme.

In fact, the current projected cost of the ‘triple lock’ stems not from one but from two reforms. When the ‘triple lock’ was introduced in 2010, it applied to the then Basic State Pension (BSP). The Additional State Pension (ASP) was to continue to be indexed to the Consumer Price Index (CPI). Hence, as I have illustrated, the BSP component would likely grow faster than the ASP. Confusingly, too, the Minimum Guarantee to the Pension Credit would continue to be uprated in line with earnings, whilst the Saving Credit component of the Pension Credit could be uprated ‘as the Secretary of State sees fit’. (House of Commons, 2016) (This simultaneous use of four different uprating systems is pretty much par for the course in UK pension policy. Of course, it makes any projection of future costs and of ‘intergenerational fairness’ highly problematic).

A key change in pension policy – which has largely been ignored by commentators on the ‘triple lock’ – was the decision in the Pension Act 2014 to introduce a new single-tier state pension in 2016, broadly merging the BSP and ASP, but then applying the ‘triple lock’ to the whole value of the combined pension. As I have said, the ASP had typically been subject to uprating in line with prices and would have tended to grow more slowly than the BSP which was subject to the ‘triple lock’. Moreover, the government set out the principle that this new State Pension should exceed the Guarantee component of the Pension Credit, and that the latter need not be uprated at a rate exceeding earnings growth, thereby reversing the relative uprating rules that were prevalent for much of the period of the previous Labour administration. It is this combination of policies, rather than the introduction of the ‘triple lock’ per se, that may contribute to the projected growing cost of state pensions. This does not seem to be well understood in some pronouncements in the media.

The future growth of prices and earnings

From a longer term perspective, given that the UK government has some rather pressing policy issues to deal with, a re-evaluation of the ‘triple lock’ should not perhaps be a priority, at least for the immediate future. The trajectory of earnings ad prices since 2010 has been unprecedented in post-war economic history (except perhaps the early 1950s). In a historical time frame, were inflation to be at the Bank of England’s target of 2%, and allowing for productivity and labour force growth of an additional 1% to 1½%, the ‘third leg’ of the ‘triple lock’ (the 2.5% minimum) would not normally be binding and a ‘double lock’ would suffice (albeit potentially still rather generous to pensioners). I am no forecaster, but to project near-zero rates of earnings growth and inflation into the future seems implausible. The Bank of England is now likely to forecast inflation rising next year to 2.5% as a result of the depreciation of the £ sterling following the Brexit decision. It is also arguable that, if Brexit actually leads to a fall in net migration, the rate of earnings growth, especially among those on below median earnings, may be somewhat higher than has been the case in recent years. This is consistent with the findings of the Migration Advisory Committee, although any forecasts on future earnings growth are probably beset by even more uncertainty than those for inflation. But it may prove to be the case that other components of the ‘triple lock’ are the binding determinants of the uprating procedure, rather than the 2.5% ‘floor’, in the coming period.

‘Intergenerational fairness’ – more comprehensive evidence needed

There is however the wider question of ‘intergenerational fairness’. Why do we have a ‘triple lock’ to protect pensioners at all, when other segments of society, such as ‘young hard-working families’ have no specific protection? Much has been made of the combination of low real earnings growth, pensioner protection and high asset prices (notably housing) that have benefited ‘the old’ at the expense of ‘the young’ since 2009. But these ‘Generational Accounts’ can only be calculated accurately on a full lifetime perspective, with full measures of intergenerational transfers (private – i.e. intra-family – as well as public). These data are not simply not yet available for younger generations, by definition. Moreover, unsurprisingly, such calculations of ‘generational fairness’ are heavily sensitive to projections of GDP, price and earnings growth (Banks, Disney and Smith, 2000).

Finally, leaving aside the current uncertainty associated with the post-Brexit UK economy, the evolution of the UK economy since 2010 has been highly unusual relative to previous post-Recession periods, being characterised by high employment growth, high asset prices and low earnings growth. More typically in the past, recovery from recession has seen faster earnings growth, higher unemployment (and hence, slower employment growth) and falls in asset prices (as have characterised many other European economies in the post-2009 period). The UK economy may indeed be embarking on a very different trajectory in the future from previous periods in terms of the evolution of real earnings and asset prices. These may herald major changes in the balance of intergenerational life chances and standards of living but it is a little early to see what these changes may be.

References:

Banks, J., Disney, R. and Smith, Z. (2000) ‘What can we learn from Generational Accounts for the UK?’ Economic Journal, (Features), 110, (November), F575-F597.

Disney, R. (2016) ‘Pension reform in the United Kingdom: An economic perspective’, National Institute Economic Review, 237 (August), R6-R14,

House of Commons (2016) State Pension Uprating, 2010 onwards, Briefing Paper No SN-05649, February 10. UK Parliament House of Commons Library.

Related Blog Posts

Related Projects

Related News

Letter to the Financial Times: Is Perfidious Albion About to Make a Return?

14 Jun 2024

3 min read

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Everything You Wanted to Know About the US Budget Deficit and Debt But Were Afraid to Ask

09 May 2024

Global Economic Outlook Box Analysis

To What Extent Has the Recovery and Resilience Facility Supported the EU Recovery from Covid?

09 May 2024

Global Economic Outlook Topical Feature

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

Related events

2024 UK General Election: The Economy and Living Standards

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum