The UK economy since the EU referendum in 6 charts

Rivers of ink will be spent on political commentary on the first anniversary of the EU referendum. We at NIESR decided to use our unique expertise to show the evolution of economy since the vote took place in six charts covering Inflation, wages and consumption, investment, housing market and equities.

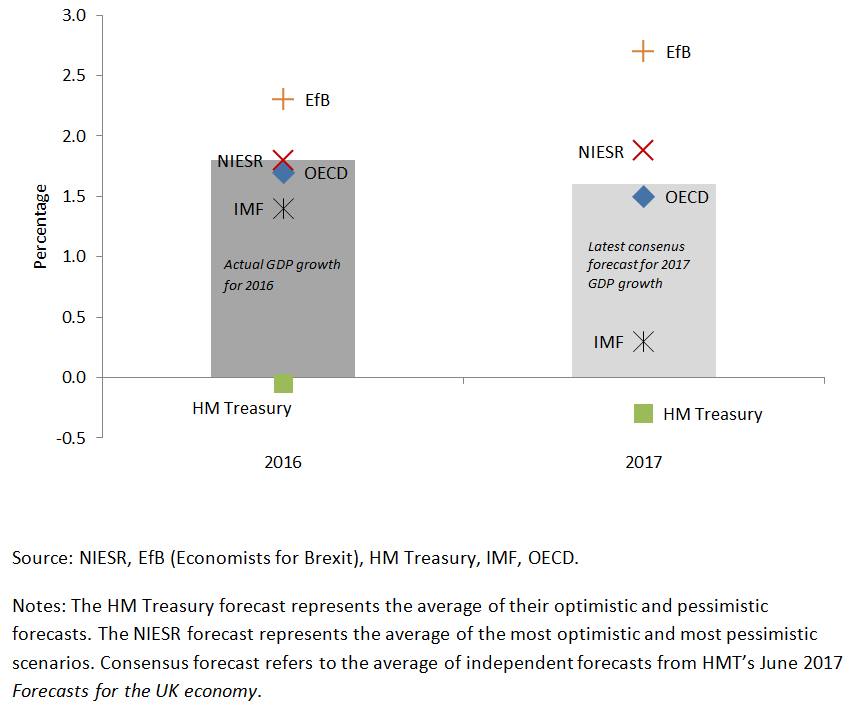

Our final chart compares GDP growth forecasts by different institutions and shows that NIESR’s own Brexit scenario for 2016 turned out to be pretty much on the money. While the outturn for 2016 was not as bad as some had feared the economy has slowed down markedly this year so far, despite robust employment growth.

Authors

Rivers of ink will be spent on political commentary on the first anniversary of the EU referendum. We at NIESR decided to use unique expertise to show the evolution of economy since the vote took place in six charts covering Inflation, wages and consumption, investment, housing market and equities.

Our final chart compares GDP growth forecasts by different institutions and shows that NIESR’s own Brexit scenario for 2016 turned out to be pretty much on the money. While the outturn for 2016 was not as bad as some had feared the economy has slowed down markedly this year so far, despite robust employment growth.

- Chart 1. CPI inflation and effective exchange rate

The depreciation of sterling since the referendum has fed through to import prices, raising consumer price inflation. We expect inflation to rise further, as rising import prices work their way through to consumer prices, peaking in the final quarter of this year.

.PNG)

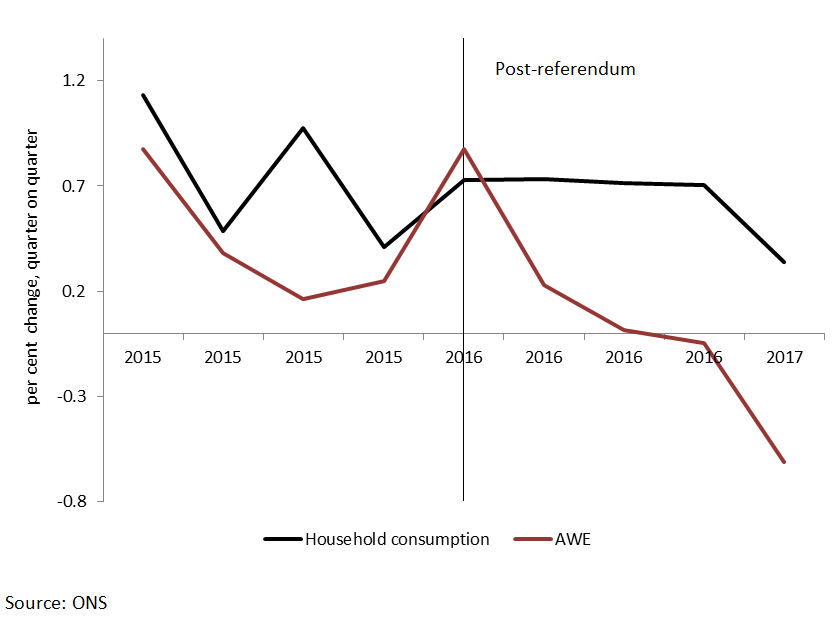

- Chart 2. Average weekly earnings and household consumption

Real household incomes have been squeezed by rising inflation. As a result consumer spending has slowed, but not to the same extent as real wages, implying a fall in the saving ratio. One positive outcome over this period is the robust growth in the number of people employed.

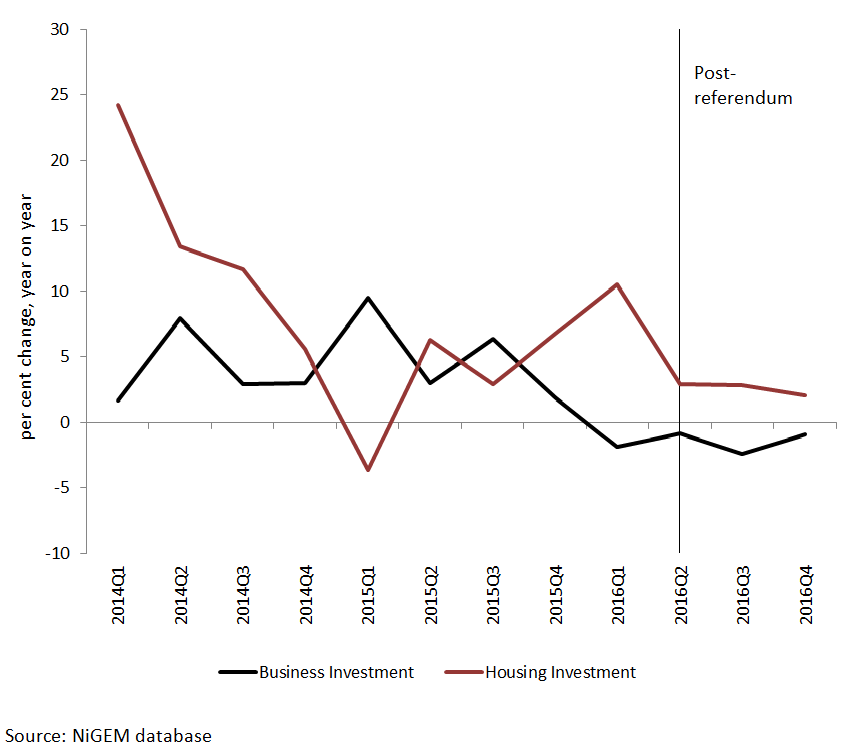

- Chart 3. Business investment and housing investment

Rising uncertainty has weighed on housing and business investment following the referendum. Business investment started to fall before the referendum, suggesting that firms were already acting with caution.

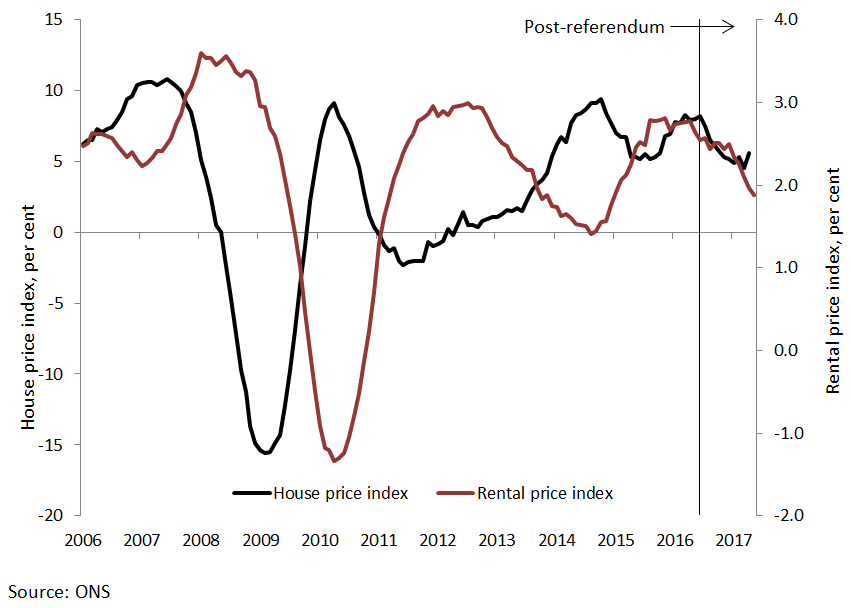

- Chart 4. House price and rental price inflation

Historically, house price and rental price inflation have moved in opposite directions. However, since the start of 2016 they have fallen in tandem. This could be a consequence of an increase in supply, or a decrease in demand due to falling real incomes.

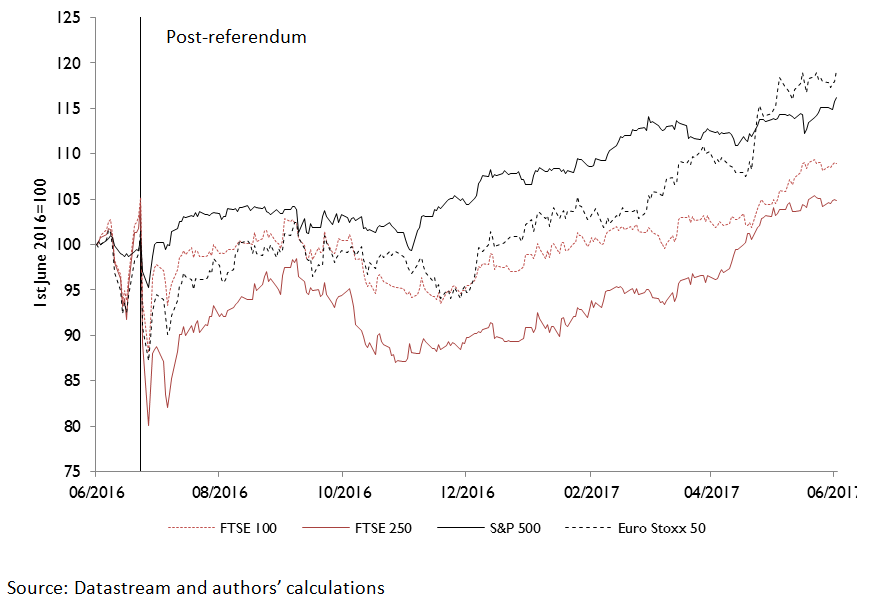

- Chart 5: Equity market prices in US dollars

The performance of the FTSE 100 in US dollar terms (to control for the effects of sterling’s depreciation) has been relatively weak compared to the S&P 500 and Euro Stoxx 50 indices.

- Chart 6: GDP growth, comparison of forecasts

GDP growth has slowed broadly in line with the NIESR Brexit scenario published in NIESR’s May 2016 Review.

Related Blog Posts

Related Projects

Related News

Letter to the Financial Times: Is Perfidious Albion About to Make a Return?

14 Jun 2024

3 min read

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Everything You Wanted to Know About the US Budget Deficit and Debt But Were Afraid to Ask

09 May 2024

Global Economic Outlook Box Analysis

To What Extent Has the Recovery and Resilience Facility Supported the EU Recovery from Covid?

09 May 2024

Global Economic Outlook Topical Feature

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

Related events

2024 UK General Election: The Economy and Living Standards

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum